The movement of money (loans) shows credit creation in business and real estate loans, which represent over 50% of total credit creation in the US, continues to contract sharply despite the efforts of QE1, QE2, and QE3 (coming).

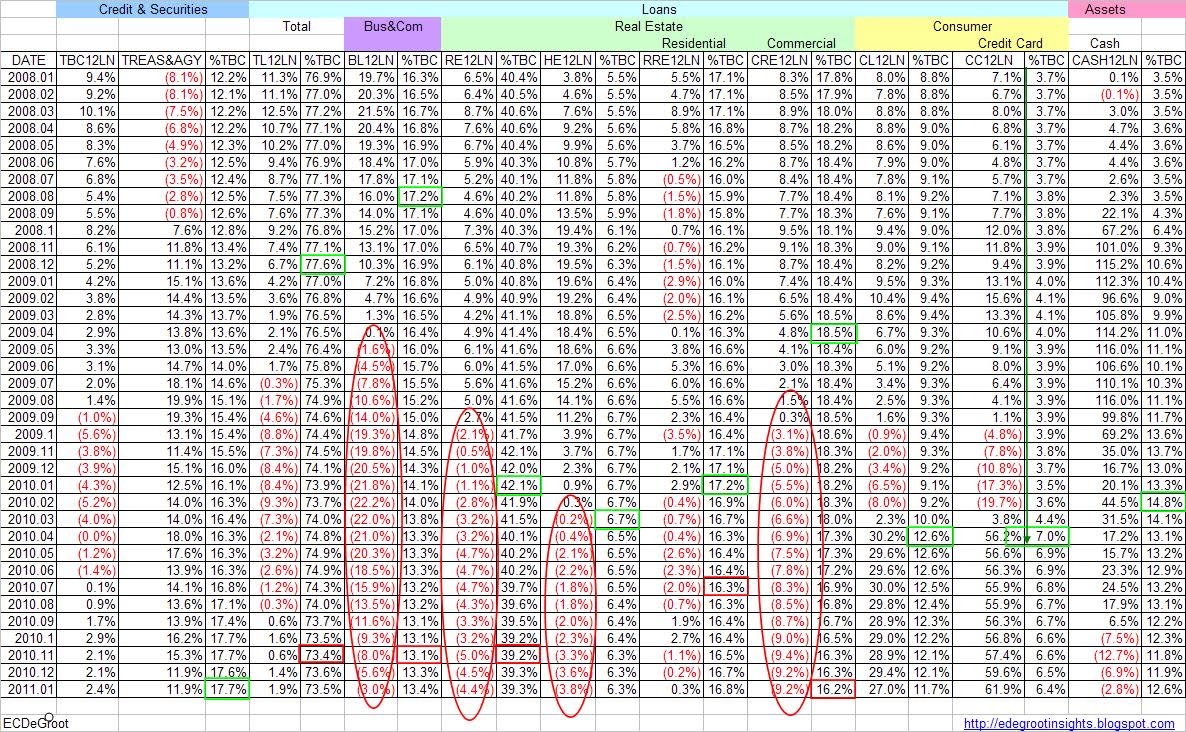

Breakdown of Total Credit At All US Commercial Banks

The following chart illustrates this sharp contraction since 2008.

Business & Commercial and Real Estate Loans Year-over-Year Change For All Commercial Banks

Perhaps, liquidity to infinity, including the Fed direct bond buying program, is motivated by market factors. Put it this way, if there's a Treasury auction and participation rates from the usual foreign buyers (China, Japan, UK, and Middle East) begins to fall, what happens? Does the US Treasury simply sell fewer bonds. That is, provide fewer dollars for deficit spending? If the answer is no, then it’s only logical that new buyer must emerge to keep the dollars flowing.

Any action that reduces the Fed's ability to participation in Treasury auctions under an environment of waning foreign demand prevents the economic can from being kicked down the road. The process of immediate finger pointing will blame those sitting in the political hot seat right now. The "adjustment process", both economic and currency-related, will not be voluntary.

Eric,

I highly value your opinion and have a question for you.

With the Fed accruing US Treasury debt en masse, what is the

possibility of that continued accumulation proceeding to dwarf other

holders' assets, then government legislating the Fed into

insignificance or reneging on obligations toward it?

Such a drastic action would undoubtedly trouble other US debt holders

without a major effort to explain the reasoning. However, it could

drain excess liquidity at the expense of an already reviled and

troubled institution - an economic and political win-win. Perhaps this

would occur after establishment of a new multi-national currency

and/or reinstating Mr. Sinclair's version of a gold ratio.

Thanks and take care,

Ramon

0 comments:

Post a Comment